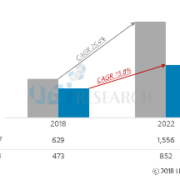

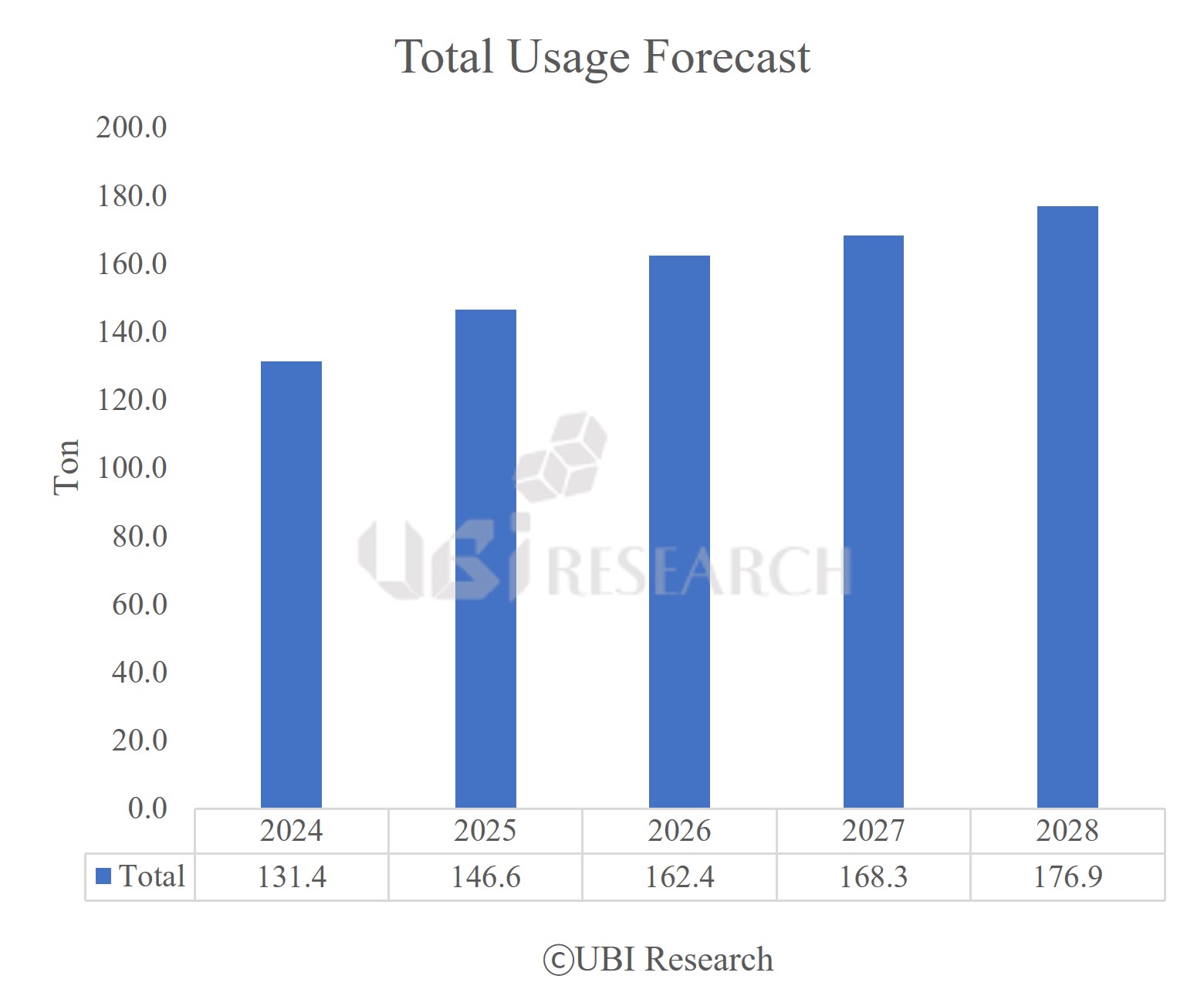

OLED emitting material demand expected to grow to 177 tons by 2028

According to the ‘2024 OLED Emitting Materials Report’ recently published by UBI Research, the total demand for emitting materials in 2024 is expected to be 131 tons, and the demand for emitting materials is expected to be 177 tons by 2028 with an average annual growth rate of 7.9%.

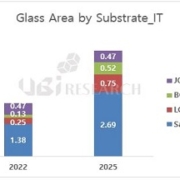

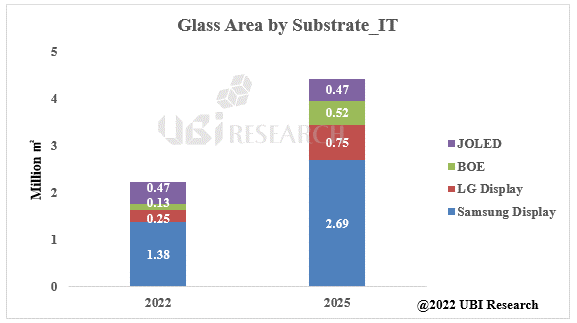

According to the report, as Samsung Electronics applied rigid OLED to its Galaxy A entry-level product, Samsung Display’s rigid OLED shipments, which were previously expected to decrease, increased. Additionally, as the application of OLED to IT devices, including iPad, expands, the demand for emitting materials is expected to increase until 2028.

The size of the OLED emitting materials market is also expected to increase. According to the report, the overall OLED emitting material market is expected to grow from $2.4 billion in 2024 to $2.7 billion in 2028.

Korean panel companies’ OLED emitting material purchases are expected to increase from $1.4 billion in 2024 to $1.5 billion in 2028, and Chinese panel companies’ material purchases are expected to increase from $980 million in 2024 to $1.21 billion in 2028.

‘The 2024 OLED Emitting Materials Report ‘ includes the latest trends in iPad Pro OLED, which recently started production, emitting material structure and supply chain, 8.6G IT line investment trend by panel company, tandem OLED emitting material development trend, and high-efficiency and long-life emitting material development trend, etc.

2024 OLED Emitting Materials Report Sample Download

2024 OLED Emitting Materials Report Sample Download