This Year’s OLED Mass Production Capacity Substrate Area is Expected to be 47.3 million ㎡

According to the ‘2022 OLED Components and Materials Report’ recently published by UBI Research (www.ubiresearch.com), a company specialized in OLED market research, the substrate area of the total OLED mass production capacity in 2022 is expected to be 47.3milion ㎡. In 2022, the LTPO TFT line and EDO’s 6th-generation rigid OLED line, which Samsung Display invested in to supplement the idle capacity of the A3 line, are scheduled to be operated. In 2023, LG Display’s E6-4 line and BOE’s B12-3 line Line, Samsung Display’s 8.5G IT line are expected to be put into operation in 2024.

As for the substrate area of small OLED for smart watch and smartphone, the line capacity for rigid OLED in 2022 is 5.29 million ㎡, accounting for 24.8% of the market share. Rigid OLED investment is not expected in the future. In 2022, the capacity for flexible OLED is 15.3 million ㎡, accounting for 71.5% of the total. From 2024, part of Samsung Display’s A3 line will be converted to an IT line, and the mass production capacity is expected to decrease. The line capacity for foldable OLED is expected to reach 0.79 million ㎡ in 2022 and 1.52 million ㎡ from 2023.

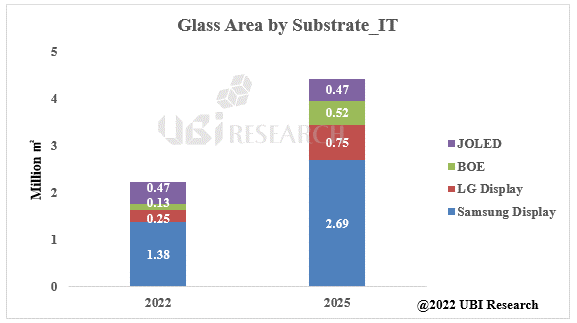

Samsung Display’s IT line capacity is expected to expand to 2.69 million ㎡ by 2025 as part of the A3 line is converted to an IT line in the first half of 2024. A new 8.5G line is expected to be operated in 2024. From the second half of 2023, LG Display’s capacity is expected to be 0.75 and 0.52 million ㎡, respectively, with the E6-4 line operating and BOE’s B12-3 line operating.

OLED line capacity for TV is not expected to change until 2026 unless additional investment is made. From 2022, LG Display’s mass production capacity is 20.3 million ㎡, accounting for 85.5% of the total. Capacity is expected to increase further depending on whether additional customers are secured in the future. Samsung Display’s capacity is 3.3 million ㎡ and BOE’s is 0.13 million ㎡, accounting for 13.9% and 0.6% of market share, respectively.

Meanwhile, the ‘2022 OLED Components and Materials Report’ published this time dealt with the latest OLED industry issues analysis, development of components and materials for foldable devices, industry status, analysis of mass production capacity of OLED panel companies, and major component and material market forecasts. It is expected to help parts and materials companies to understand related technologies and predict future technology directions and markets.