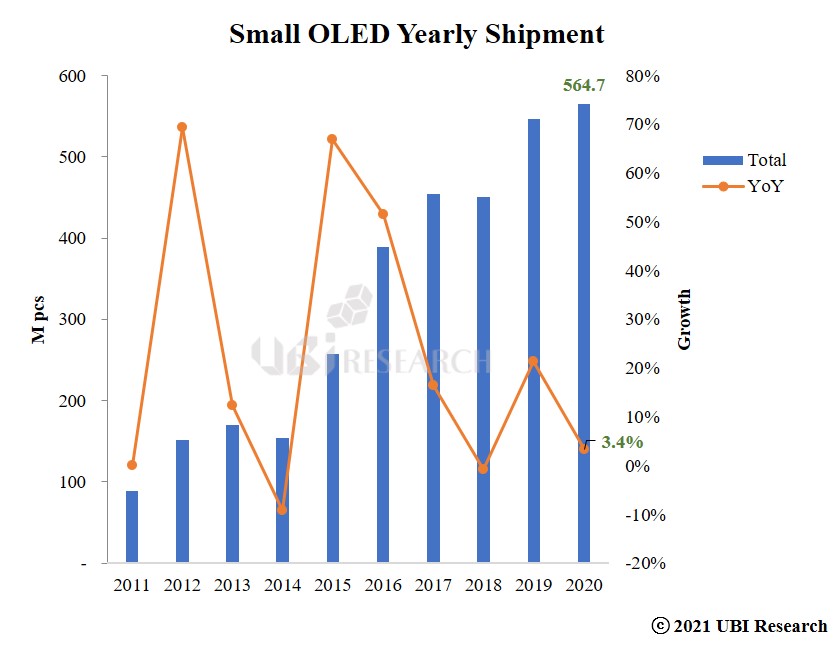

According to “3Q22 Small OLED Display Market Track” published quarterly by UBI Research, the market for small OLED displays in the second quarter of 2022 was estimated at $7.87 billion.

In the second quarter of 2022, the OLED small display market decreased by 16% compared to the previous quarter and increased by 9.7% compared to the same quarter last year. The Chinese market, the world’s largest market, has shrunk mobile devices shipment as Shanghai and some regions were quarantined due to COVID-19.

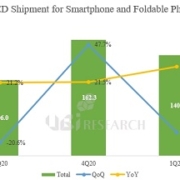

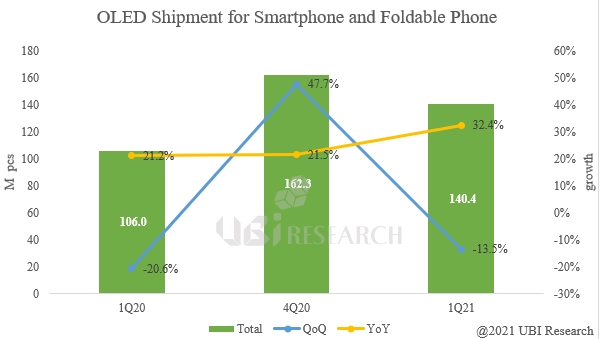

As a result, shipments of small OLED panels decreased from 150 million units in the first quarter to 130 million units in the second quarter. Although shipments of foldable OLED panels in the second quarter increased by 120,000 units from the first quarter to 3.12 million units, the market size fell short of expectations.

Small OLED market in 2Q 2022

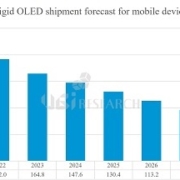

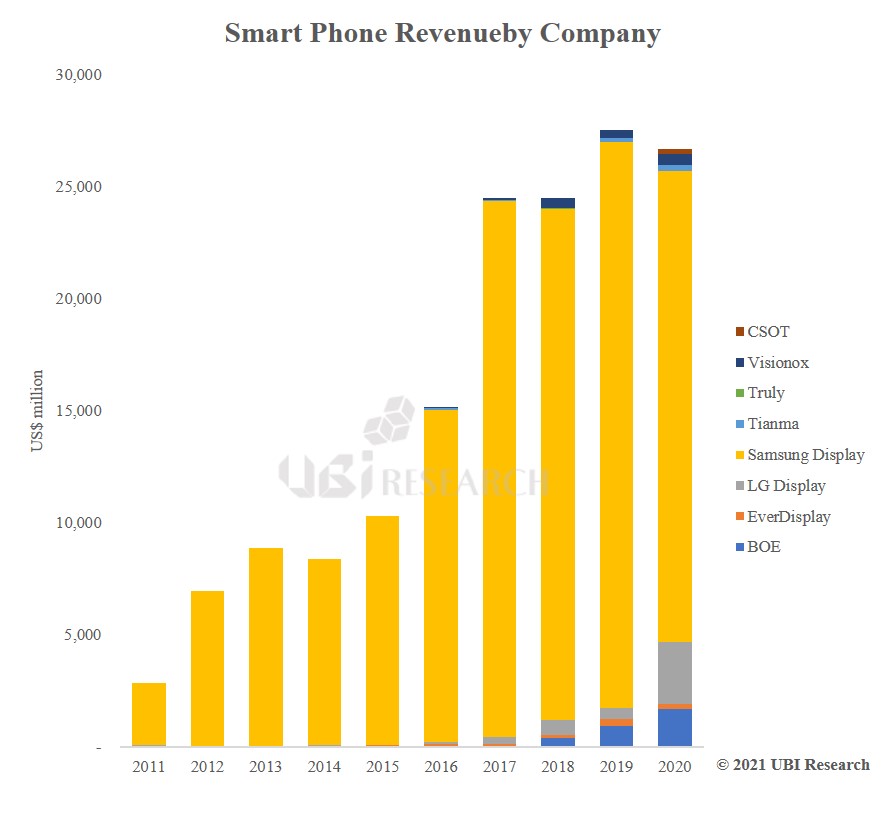

As some Chinese panel manufacturers are offering OLED panels for Smartphones below $30 recently, the rigid OLED market is expected to shrink rapidly.

It is predicted that shipments of foldable OLEDs will increase 6.1 million units from 10.3 million units last year to 16.4 million units this year. Although foldable phones are expected to replace Samsung Electronics’ Galaxy Note, there is no additional demand. In addition, it is predicted that the growth rate of foldable OLED markets will not be fast, due to Chinese panel manufacturers’ difficulty in purchasing UTGs for foldable OLEDs and it is affecting Chinese smartphone manufacturers’ production. In 2027, OLED shipments for foldable phones were significantly revised to 42 million units.

Small OLED display shipments by application (Watch, Smartphone, Foldable Phone) and the estimated shipments by 2027 are shown as a 100% cumulative graph.

Small OLED Shipments and Forecasts in 2Q 2022

Total shipments of small OLED display panels are expected to be 724.8 million units in 2022, and it is estimated that it will reach 937.8 million units in 2027. The proportion of foldable phones by application product in 2022 is 2.3% and is expected to increase to 4.5% by 2027.

“3Q22 Small OLED Display Market Track” analyzed OLED production capacity status for small OLED displays below 10 inches, and surveyed quarterly sales and shipments of major products sorted by major panel manufacturers, countries, generations, substrates, TFT technologies, and application products(Watch, Smartphone, Foldable phone). It analyzes ASP and OLED demand/supply by application and provides data on market prospects of small OLED displays from next 5 years to 2027.

3Q22 Small OLED Display Market Track Sample Download

3Q22 Small OLED Display Market Track Sample Download