Foldable and slidable OLEDs are replacing LCDs in IT

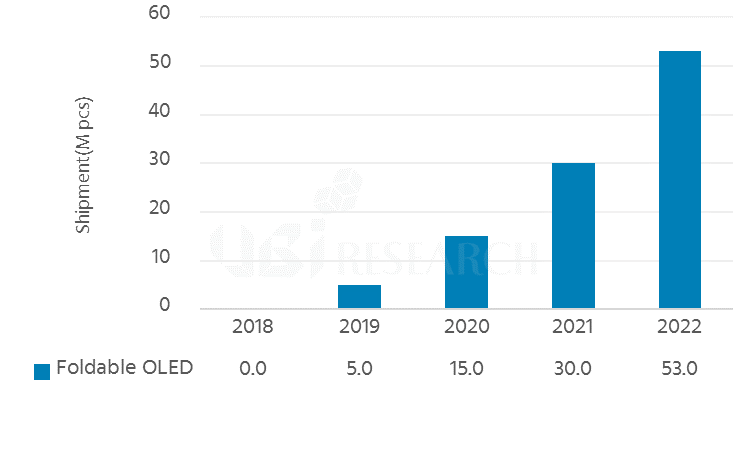

Foldable OLED technology, which started in the smartphone market, is also sprouting up in the notebook market. Foldable OLED technology has the advantage that the entire front of a smartphone or notebook can be configured as a screen, and since the screen can be folded, it is a product that enhances portability. Therefore, it will become an essential product in the increasingly sophisticated information age.

Notebooks are the optimal application of Foldable OLED because the form factor itself is a foldable product, and since folding phones have existed in the mobile phone market before, foldable phones are also naturally being incorporated into the lives of modern people. Since the foldable book can be expanded to 20 inches, it will evolve into a new product that can overcome the monitor market.

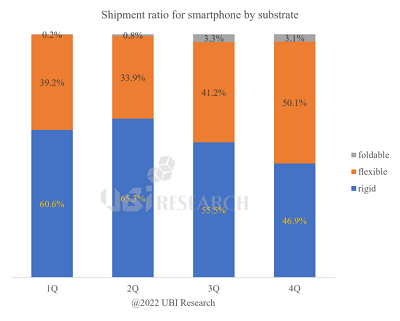

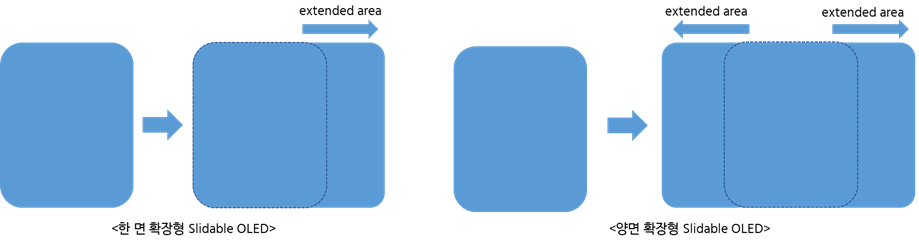

Following on the heels of foldable OLED technology is slidable OLED. Slidable OLED is a way to expand the screen by taking out the OLED inside the device. Like Foldable OLED, Slidable OLED is a technology that can expand the screen, making it more portable. The application of Slidable OLED is a slidable PC that will replace tablet PCs. Instead of a 13-inch tablet PC, a slidable PC that can expand to 17 inches will be a new product that can expand to the notebook market.

Foldable Book and Slidable PC will be a game changer that will break the boundaries of the IT market where LCDs are used.

Originally published in 2024, the report “Foldable & Slidable OLED Technology and Market Outlook” detailed the technologies that are essential for foldable and slidable OLEDs to succeed in the market and provided a forecast of the future market.

Foldable & Slidable OLED Technology and Market Outlook Report Sample

Foldable & Slidable OLED Technology and Market Outlook Report Sample