Dr Choong Hoon Yi, UBI Research Chief Analyst, ubiyi@ubiresearch.co.kr

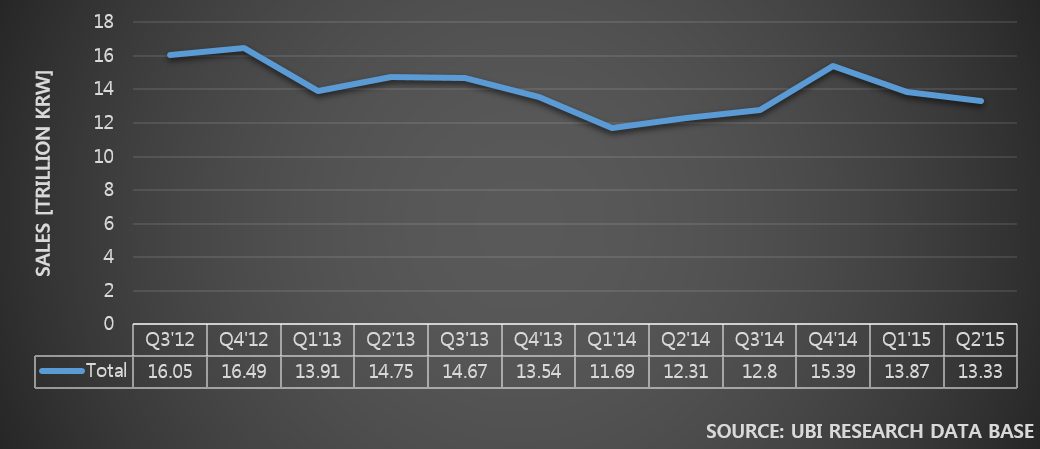

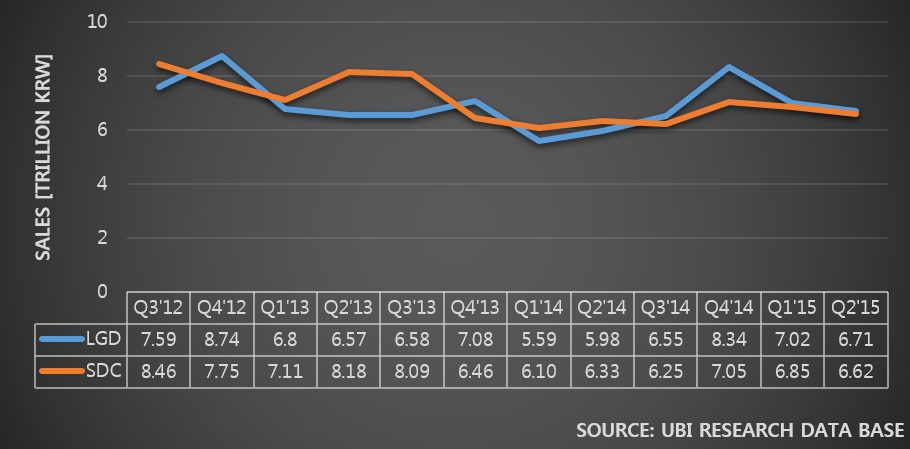

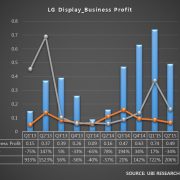

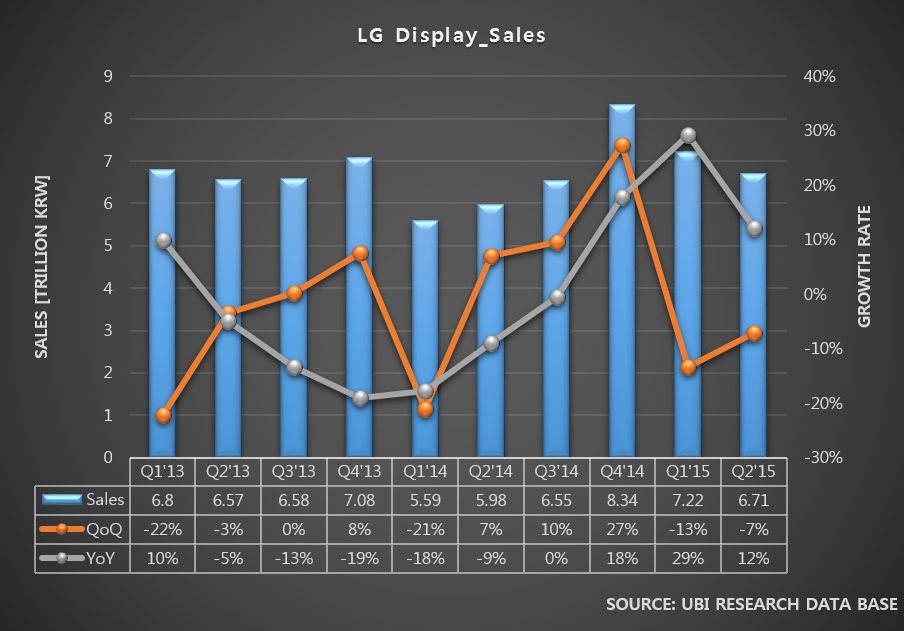

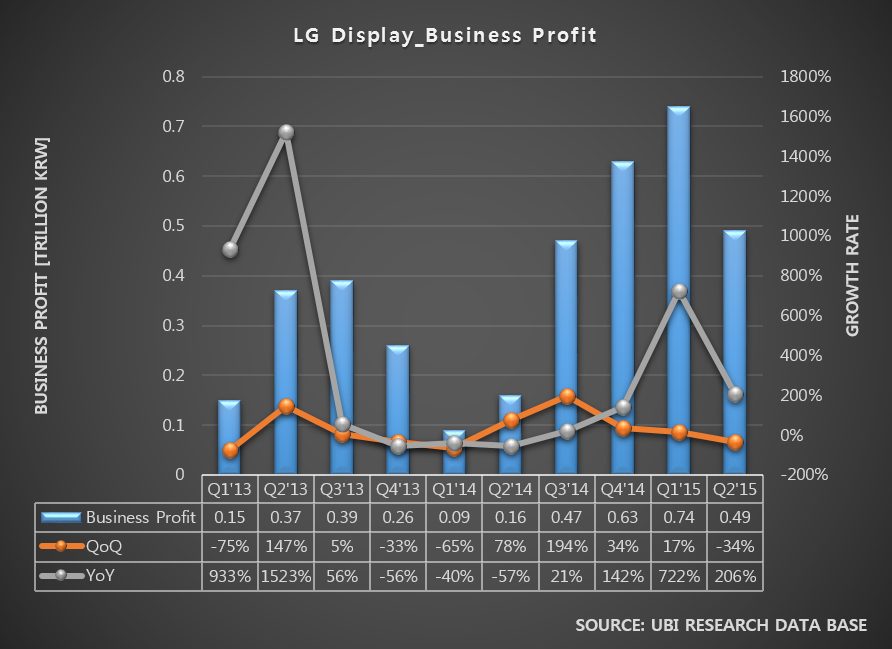

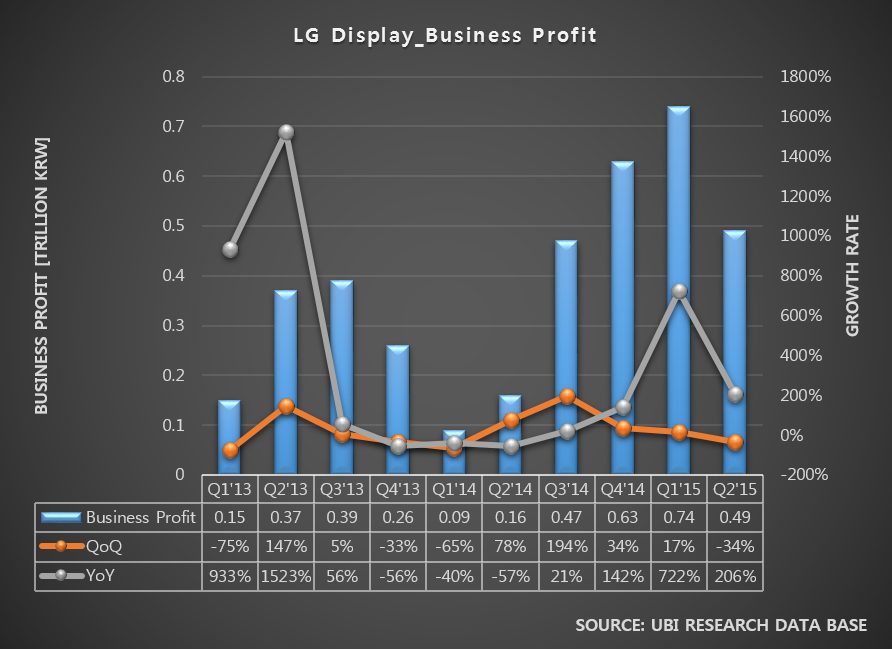

On July 23, LG Display announced its earnings results at LG Twin Towers in Yeouido, South Korea. LG Display reported that their Q2 sales recorded approximately US$ 5,700,000,000 with business profit of approximately US$ 420,000,000.

Although sales fell by approximately US$ 260,000,000 (-5%) compared to the previous quarter, it was an increase of US$ 620,000,000 (12%) compared to the year before. Business profit showed approximately US$ 210,000,000 decrease (-34%) QoQ, and YoY US$ 280,000,000 increase (206%).

LG Display’s sales and business profit of Y/Yo (green line) showed U shape of trend of growth in previous 5 quarters but this quarter recorded a fall. It is analyzed that the growth could slow down from 2H 2015.

The drop of the LG display’s Y/Yo growth in this 2Q is much attributed to smartphone market’s slow down and TV market reduction. It is also estimated the panel price reduction due to Chinese display companies’ aggressive investment is reflected.

For LG Display to stop the degrowth, mass production of products that are differentiated from competition, is urgently needed, away from LCD panel that is LGD’s current major business.

On the day, LG Display’s management announced approx. US$ 900,000,000 investment for Gen6 flexible OLED line in order to lead flexible OLED market. The investment location is Gumi factory. Investment location is Gumi factory with the initial investment of 7.5K. It is expected world’s second flexible OLED exclusive line will established following Samsung Display. It is anticipated that up to 15K will be established for this line.

Considering last year’s LG Display’s business profit was approx. US$ 1,100,000,000, the US$ 900,000,000 flexible OLED investment is very large. The investment decision must have been very difficult. However, the reasons for LG Display’s drastic flexible OLED exclusive line investment are because companies that produce LTPS-TFT LCD (LGD’s existing main market) is increasing, and because Samsung Display is already monopolizing rigid OLED market and therefore difficult to secure market share.

LG Display’s CFO Kim Sang-don explained that flexible OLED Gen6 line investment was decided at the board of directors meeting on July 22, and was made official on the morning of July 23. Kim added that the decision was reached so that LG Display can lead the OLED business in terms of technology and to occupy initial market in foldable and rollable technologies. He also commented the monthly capa. of the flexible OLED line will be 7.5K.

Regarding large area OLED panel, it was emphasized that this year’s panel production target remains to be 600,000 units and 1,500,000 units next year, same as the ones announced during the Q1 earnings results presentation. It was also revealed that 34K, approximately 9K higher than current capa., will be in operation in 2016. Addressing the concern of oversupply of next year’s 1,500,000 units while the OLD TV market is still small, LG Display suggested the solution of increasing the demand by active promotion from the second half of this year.

Despite the fall of mid to large size panels’ sales price, from the enlargement of sets and AIT technology applied sales performance, the business profit of approximately US$ 4,000 million was recorded. This is a 34% decrease compared to the previous quarter but a 199% increase from the same period in 2014. LG Display estimates that the sales will increase in the third quarter due to seasonal factors and panel’s enlargement trend.